China’s relationship with the Gulf Cooperation Council (GCC) countries has changed profoundly in decades past. What began as a relatively narrow relationship – shaped by diplomatic recognition and basic trade – has evolved into one of the most economically consequential partnerships in the wider Middle East. This evolution accelerated sharply once China became a net oil importer in the 1990s, shifting the relationship from one marked by ideological distance to one ofpragmatic economic engagement.

Today, China’s footprint across Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) is no longerdefined solely by oil purchases. It is increasingly visible in ports and logistics, infrastructure construction, power plants, industrial parks, renewable energy-supply chains, and the digital economy. While the relationship has become more comprehensive, it remains bounded by an enduring structural reality. In Gulf strategic thinking, China is an increasingly important economic partner, while the United States remains the central security provider.

It was this so-called division of labour – economic deepening without security substitution, albeit accompanied by a growing diplomatic footprint – that brought the East Asian Institute (EAI) and the Middle East Institute (MEI) together to examine the durability and the limits of China–Gulf relations. Yet the ongoing geopolitical dynamics in the Middle East could reshape thisrelationship in important ways going forward, with potentially significant implications for China–GCC ties.

Complement, Not Substitute

While the Gulf states value China as a development partner and a source of strategic flexibility, this relationship is shaped less byBeijing’s growing presence than by how GCC states integrate China into existing economic and security frameworks.

Enduring security dependencies and regional calculations mean that the GCC approach is one of “complementarity, notsubstitution”. The clearest ceiling on China’s role in the Gulf is security. There is little expectation that deepening economic ties willtranslate into a fundamental strategic realignment away from the United States. Security guarantees, advanced military capabilities, and crisis management remain overwhelmingly linked to Washington. The United States remains the primary security guarantor in the region with a robust network of bases, defence agreements, and arm sales, while its arms sales and technology transfers constitute the major pillar of this partnership.

With limited power-projection capabilities, China is unable to become a security provider. In addition, given Beijing’s guiding foreign-policy principle of non-interference, it is unwilling to take on the role. Instead, it prefers to advocate regional solutions rather than assume external leadership.

Energy Remains the Anchor Despite Diversification

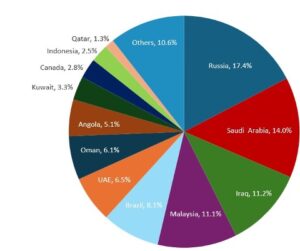

Energy remains at the core of China’s GCC engagement despite its diversification beyond oil purchases. The Gulf states are crucial to China’s domestic energy needs and security, supplying 31.2% of China’s oil imports in 2025, with Saudi Arabia and the UAE playing particularly important roles in ensuring stable energy flows (see Figure 1). That said, the energy relationship has also evolved over the years, and this is no longer just about crude oil shipments. Sino-GCC energy ties are increasingly reinforced through long-term contracts, joint ventures, and downstream industrial integration in refining, and petrochemicals.

FIGURE 1 CHINA’S MAIN CRUDE OIL SUPPLIERS IN 2025

Source: China’s General Administration of Customs.

Energy cooperation is also broadening amid the global energy transition. The scope of bilateral ties now includes clean-technologyand renewable-energy equipment, with Gulf states leveraging China’s manufacturing capabilities to advance their net-zeroambitions. This matters because it signals a shift from a relationship built on hydrocarbons alone to one that increasingly spans both the old and the new energy economies.

From Ideological Distance to Pragmatic Economic Alignment

Historically, China’s engagement with the Gulf was limited. The initial stages of the relationship during the 1990s largely focused on diplomatic recognition and basic trade relations. That began to change as China’s imports of oil and gas from the Middle East increased substantially over the past three decades, with China’s rise as a major global economic power reinforcing this shift. As China’s global economic weight increased, its ambition to expand outreach to the Gulf grew in parallel.

In this context, China’s economic diplomacy in the region has been proactive and multi-instrumental, involving trade, investment, infrastructure financing, and construction. The drivers are clear and consistent: meeting domestic energy demand, expandingoverseas markets, and securing investment and infrastructure opportunities.

Planning-Horizon Alignment

A central structural reason the China–Gulf partnership has deepened so rapidly is alignment in planning horizons between both sides. Each GCC state has articulated a long-term national-development blueprint aimed at reducing dependence on hydrocarbons, modernising national economies, and building more sustainable and knowledge-driven growth models. These strategies form the backbone of the Gulf’s transition toward diversified post-oil futures.

These long-term frameworks find in China a partner aligned with ambitions for structural economic change. In practical terms,China’s strengths – for instance, scale economies, long-horizon economic engagement, and large-project delivery – fit naturally with GCC states’ national visions (e.g. Saudi Vision 2030, Kuwait’s Vision 2035, and Qatar’s National Vision 2030), which in turnaligns with China’s Belt and Road Initiative. This compatibility helps explain why cooperation often advances smoothly, even when geopolitical tensions rise elsewhere.

Sectoral Broadening

While energy remains the anchor of their ties, China’s engagement with Gulf states has expanded well beyond hydrocarbons. The relationship now includes infrastructure, clean technology, and digital technology. China has positioned itself as a key player in a changing regional landscape by steadily expanding its economic footprint into sectors such as manufactured goods, greentechnology, and the digital economy.

This sectoral broadening is not accidental. It reflects a strong alignment between what China can offer and what the GCC states increasingly demand. Gulf Cooperation Council states are undertaking significant reforms and multi-decade development visions aimed at economic diversification and sustainable growth. Theseambitions align with China’s strengths in technology, infrastructure delivery, and industrial development.

China’s shift from high-speed to quality-driven growth has reshaped its economic engagement with the GCC. Industrial upgrading in China has encouraged outward investment into new sectors and markets, including the GCC countries. Nevertheless, China’sdomestic economic slowdown since 2018 introduces uncertainty for GCC exports, especially energy.

At the same time, the GCC states increasingly see China not simply as a buyer of hydrocarbons, but as a partner in industrialisation,infrastructure development, and technological upgrading. Chinese firms are valued for scale, speed, and cost efficiency in sectors such as logistics, manufacturing, renewable energy, and digital infrastructure.

From State-Owned Enterprises to Private Firms: A Clear Shift in China’s Model

One of the most important changes in China’s GCC engagement has been the evolution of its corporate footprint. The earlier engagement was dominated by large Chinese state-owned enterprises (SOEs), particularly in infrastructure construction and energy. Key actors have included China Petroleum and Chemical Corporation (more commonly known as Sinopec), China National Petroleum Corporation, Power Construction Corporation of China, China State Construction Engineering Corporation, and China Energy Engineering Corporation. Concrete examples illustrate this pattern. The China Ocean Shipping Company is involved in port and transport-linked projects such as the Jazan Port initiative in Saudi Arabia. Similarly, the China Gezhouba Group is contracted for large infrastructure works in Kuwait’s South Saad Abdullah New City, including roads, pipe networks, lighting, and irrigationsystems.

In recent years, however, China’s footprint has diversified and shifted toward a broader mix that includes large private firms,particularly in technology and the green economy. Huawei Technologies, Alibaba Group, and Zhongxing Telecommunication Equipment Corporation are prominent examples, and their engagements in the Gulf are linked to cloud and data centre infrastructure, artificial-intelligence (AI) applications, and smart-city initiatives across Kuwait, Saudi Arabia, and the UAE. A flagship example is Huawei’s cloud-data centre project in Saudi Arabia, which is linked to accelerating digital transformation as well as the adoption of cloud and AI technologies across government and public services.

This corporate transition – from state-led infrastructure delivery to private-sector digital platforms and advanced technology – signalsa broader shift in the relationship itself. China is no longer only building the Gulf’s physical infrastructure; it is also increasingly helping shape the region’s digital and technological infrastructure.

Trade Expansion: The Gulf as a Growing Destination for Chinese Exports

Sino-GCC bilateral trade has expanded steadily over the past two decades, and the Gulf has become a more important destination for Chinese exports and import source for China. Saudi Arabia and the UAE dominate bilateral trade flows, reflecting their dual roles as major energy suppliers and regional trade and logistics hubs.

This trade expansion reinforces a key point: China’s GCC engagement is not only about importing energy. It is also about exportingmanufactured goods, technology, and increasingly, services linked to digital infrastructure and industrial upgrading.

The Belt-and-Road Initiative

The Belt and Road Initiative (BRI) has transformed China–GCC relations, with the GCC becoming a key node in China’s global connectivity vision. All GCC states have signed BRI cooperation agreements, enabling implementation of large-scale infrastructure and energy projects.

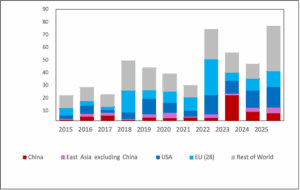

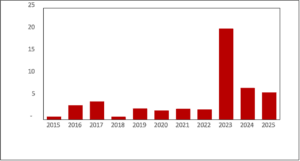

Announced greenfield investments in GCC countries from China rose significantly in the last three years, averaging US$13 billion between 2023 and 2025 (see Figures 2 and 3 below). Two-thirds of China’s announced investments in the GCC were in manufacturing activities, namely the metals, electronics, and renewable energy. This aligns with China’s expanding engagement with the GCC in recent years.

FIGURE 2 GREENFIELD FDI ANNOUNCEMENTS IN THE GCC, 2015–2025

Source: Financial Times’ fDi Markets.

FIGURE 3 CHINESE GREENFIELD FDI ANNOUNCEMENTS IN THE GCC, 2015–2025

Source: Financial Times’ fDi Markets

Deepening Institutionalisation: Bilateral and Multilateral Frameworks

China–GCC relations are no longer ad hoc, but increasingly institutionalised. Bilaterally, China has established strategicpartnerships with most GCC members, notably Saudi Arabia and the UAE. Multilaterally, mechanisms such as the China–Arab States Cooperation Forum (established in 2004), and the China–Gulf Cooperation Council Strategic Dialogue (established in2010), have deepened cooperation in trade, investment, technology, and culture.

These institutions provide coordination frameworks and signal long-term commitment, even though bilateral relations remaincentral. While multilateral platforms complement bilateral relations between China and the GCC states, they lack binding commitments.

Conclusion

China’s ties with the GCC countries have moved well beyond an oil-for-goods relationship into a broader, increasinglyinstitutionalised economic partnership spanning infrastructure, transport, green technology, and the digital economy. Yet the structure remains clear: energy and trade provide the foundation, investment is diversifying from SOE-led construction towards a wider mix that includes major private technology firms, while the long-horizon Gulf transformation agendas create a natural fit with China’s development-oriented engagement.

The United States remains the decisive – and indispensable – power in the region, while China prefers facilitation over enforcementin regional diplomacy. Politically low-risk and predictable, this approach is consistent with sovereignty-sensitive Gulf preferences. Yet the region’s security volatility, China’s

own domestic economic slowdown, and US pressure on Gulf states not to deepen high-tech ties with Beijing, could all impact China’s ties with its GCC partners These forces may, in turn, be further amplified by the evolving geopolitical dynamics in the Middle East.

The collaboration between the East Asian Institute and the Middle East Institute seeks to provide deeper insight into these dynamics going forward, including their implications for international relations, shifting economic and sectoral patterns, institutional mechanisms, and Gulf perceptions of China’s ambitions and constraints.

Image Caption: Chinese President Xi Jinping and United Arab Emirates President Sheikh Mohammed bin Zayed Al Nahyan shake hands following a signing ceremony at the Great Hall of the People in Beijing on 30 May 2024. Photo: AFP

About the Author

Alfred Schipke is EAI Director and Professor at the Lee Kuan Yew School of Public Policy, as well as former IMF Senior Resident Representative for China; Michelle Tea is MEI Executive Director; Yu Hong is Senior Fellow at the EAI; Fang Goo is Research Fellow at the EAI; and Lin Jing was a Research Fellow at MEI