As the impasse over the war against Iran drags on, both sides appear to have dug entrenched positions, and talks to end the conflict have not made progress. Instead, both sides have declared victory, and traded threats. While the fragile ceasefire has lowered the immediate temperature in the Gulf, it has not restored certainty. For international businesses operating in the Gulf, this is an important distinction.

The region has banked its future on economic transformation programmes that require stability to attract investments and open up new growth sectors to prepare for a post-oil era, but the current war has upended the image of the Gulf as an oasis of calm in a turbulent region. This, in turn, has given rise to conversations about the future of foreign businesses – including Singaporean ones – in the Gulf, and whether they should rethink their operations there to mitigate risk.

Singapore has a substantial commercial relationship with the Gulf states. Bilateral trade in goods with the United Arab Emirates reached S$24 billion in 2024; more than 600 Singapore firms operate there, and Singapore’s direct investment into the UAE stood at S$4.9 billion in 2023. The Singapore Business Federation said business enquiries to set up in the Middle East have risen more than five-fold in the past two years. As with other economies exposed to the Gulf crisis, how Singapore firms engage with their Gulf partners during the current turmoil will be a factor that determines how the relationship will play out in the future.

This is because in Gulf business environments, competence is rarely judged in isolation. A firm can deliver technically and still weaken its standing if it does not maintain trust with its local Gulf partners. Personal relationships built on a solid foundation of trust go hand in hand with commercial performance. They shape who gets flexibility, who is given the benefit of the doubt, and who is still seen as worth backing when conditions tighten.

A Spectrum of public Responses During the War

No major foreign firm with serious Gulf exposure has executed a clean exit from the region since Operation Epic Fury began. That said, all foreign and cross-border firms in the Gulf have responded in different ways to the war.

Maritime carriers split between hard suspensions and adaptive rerouting. Some halted cargo bookings entirely and diverted shipments to safer ports, invoking force majeure clauses. Others rerouted vessels around longer but more secure corridors before gradually restoring partial flows through multimodal arrangements. Aviation responses were similarly graded: Major regional carriers suspended operations at the height of the disruption, but several resumed limited services once airspace conditions stabilised.

In finance and professional services, Citigroup and Standard Chartered evacuated Dubai offices, HSBC closed all Qatar branches until further notice, and Goldman Sachs moved regional staff to remote work. PwC shut offices across Saudi Arabia, Qatar, the UAE, and Kuwait. In industry and energy, firms implemented partial production shut-ins where necessary while keeping other operations running. TotalEnergies shut approximately 15 per cent of its Gulf productionwhile maintaining UAE onshore operations. Technology firms shifted to remote work, encouraged workload migration, or temporarily closed local offices.

The record is not one of mass exit. It is a documented spectrum of suspensions, reroutes, remote work, temporary relocation, postponements, and selective continuity measures.

This evidence base is necessarily incomplete. Large firms leave public traces through disclosures, advisories and press coverage. Small and medium-sized enterprises — which account for 95 per cent of all companies operating in the UAEand the overwhelming majority of the 600-plus Singapore firms there — are far less visible in public reporting. However, it is reasonable to assume that they were badly affected as well because of shipment delays, cost increases, and operational adjustments. The absence of systematic data does not imply the absence of impact. It reflects the limits of visibility.

The responses of firms to the tumult give rise to a key question: As Gulf states emphasise their economic staying power amid conflict, highlighting companies that have battened down the hatches, how will they view those that made for the exits? Among firms that still retain discretion in how they respond, what kinds of conduct preserve future cooperation, and what kinds damage it? This is what the relational-contract literature helps make intelligible.

Crisis Conduct and the Repricing of Credibility in the Gulf

Indeed, in markets where relationships coordinate what contracts cannot fully substitute for, commercial actors interact repeatedly, not just once.

Today’s conduct shapes tomorrow’s beliefs. Tomorrow’s beliefs shape future willingness to cooperate, share information, offer flexibility, and absorb friction. This is the logic of a game theory term called the repeated signalling game. Since staying during a crisis is costly — operationally, financially, and reputationally — it is a credible signal that a firm is a serious, long-term partner rather than a fair-weather entrant.

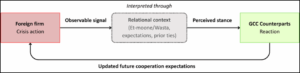

As mentioned, the Arab cultural approach is a critical component in the game. In relationship-intensive Gulf commercial environments, crisis conduct is not a footnote to the business relationship. It is a data point that updates beliefs about reliability, commitment, and future value as a partner. Two concepts from literature on international business culture are important here: Et-Moone — the relational permission and informal elasticity that accumulates between trusted counterparts over time — and the broader observation that in these environments, access flows through people rather than institutions, which is wasta. In plain terms, communication, burden-sharing, treatment of partners, treatment of local staff, and the degree of maintained presence all become legible signals (fig. 1).

Figure 1: Signalling under constraint: how crisis conduct updates counterpart beliefs in repeated commercial relationships.

As one chief executive officer of a Riyadh-based e-commerce firm put it, reflecting on the behaviour of an American technology partner during the crisis: “What stood out for us was [this partner’s] frequency of contact. They remained consistently in touch to check whether additional, emergency support might be needed, even though we did not require it — thank God.”

A chief technology officer of an Emirates-based Artificial Intelligence (AI) company operating in content infrastructure noted: “Due to the current regional situation, we are experiencing delays in hardware deliveries from Asia, and several foreign partners have postponed services until conditions stabilise.” He was clear, however, that the postponements had not damaged trust: “They communicated early that these decisions were driven by temporary external factors. We understood and appreciated those signals.”

The Gulf is Already Recalibrating

The relationship between foreign firms and Gulf markets is not one-directional. Gulf actors are not simply investment sinks; they are reallocating capital and deepening positions in foreign countries, especially in Asia, and forming their own judgments about which partners look serious in a less stable environment.

The structural shift was already underway before the Iran war. Deloitte estimates that Gulf sovereign wealth funds deployed US$82 billion globally in 2023, and another US$55 billion in the first nine months of 2024, with US$9.5 billion flowing into China alone during the latter period. The same pattern is visible in specific deals. In September 2025, Singapore’s GIC and the Abu Dhabi Investment Authority led a US$1.6 billion investment in Vantage Data Centers’ Asia-Pacific platform, including expansion into Johor. This is beyond Gulf money simply seeking a return. Gulf and Singaporean capital is already co-building regional digital infrastructure. Singapore businesses are, therefore, already part of the same regional investment map.

The Gulf Now Sits Inside Singapore Inc

The investment asymmetry is even clearer in the Singapore food and logistics sector. In February 2025, Salic, the Saudi Agricultural and Livestock Investment Company wholly owned by the Public Investment Fund, agreed to increase its stake in Olam Agri to 80.01 per cent for US$1.78 billion, with a call option on the remaining 19.99 per cent within three years. This was not a portfolio footnote, as it placed a state-linked Gulf investor at the centre of a major Singapore-linked agri-business platform.

The wider flow data point in the same direction. UAE investment into Singapore reached S$10.7 billion in 2023, up 83 per cent year on year and more than double Singapore’s corresponding investment into the UAE. That changes the strategic context. When Singapore-linked firms manage their Gulf exposure, the signal does not stop at a single customer or partner. Over time, it can also shape how Singapore-linked opportunities are read by Gulf capital.

What Singapore Businesses Should Think About Now

This is not an argument that firms must always stay. It is one for separating conduct that is genuinely discretionary, and that which is not. Security and logistics teams will decide when a route reopens, when staff can return, or when shipments resume. However, senior management has a different question to answer: What did our firm already signal to our counterparts, and what do we need to demonstrate now?

Firms that preserve credibility under constraint are better positioned for the re-engagement conversations that will eventually take place. The relevant variable is not physical presence alone, but how firms behave when constraints bind: Whether they communicate early, share or shift losses, protect local staff, or maintain some operational signal even at a reduced scale. These actions are observable. They shape how their Arab counterparts update their beliefs, not in abstract terms, but in practical ones: Whether the firm is a reliable long-term partner or a fair-weather entrant.

For Singapore, the stakes are higher than any one firm. The ASEAN-GCC Joint Declaration on Economic Cooperation adopted in May 2025 explicitly recognised the growing role of sovereign wealth funds and the need for deeper investment cooperation. Singapore will assume the Asean chair next year. A country that wants to help shape the next phase of GCC-Asean commercial ties cannot treat credibility as a soft variable. In the Gulf, it is part of the commercial architecture itself.

Image Caption: An Emirates Boeing 777 aircraft prepares for landing as a smoke plume rises from an ongoing fire near Dubai International Airport in Dubai on 16 March 2026. Photo: AFP

About the Author